A data center moratorium is not an energy policy. Neither is a pledge.

April 28, 2026 - Lancaster, PA

I live in Lancaster County, Pennsylvania. The Coreweave campuses Governor Shapiro announced last summer sit down the road. One is less than a mile away. In that same event, Pennsylvania pledged $100 billion in AI investment. Yet, State Sen. Katie Muth has filed a memo for a three-year hyperscale moratorium. I do not want the pause. I want the policy that lets Pennsylvania participate.

Sources: Reuters factbox (April 24, 2026), Good Jobs First, datacenterbans.com, MultiState. PJM territory per PJM Interconnection. Status as of April 27, 2026.

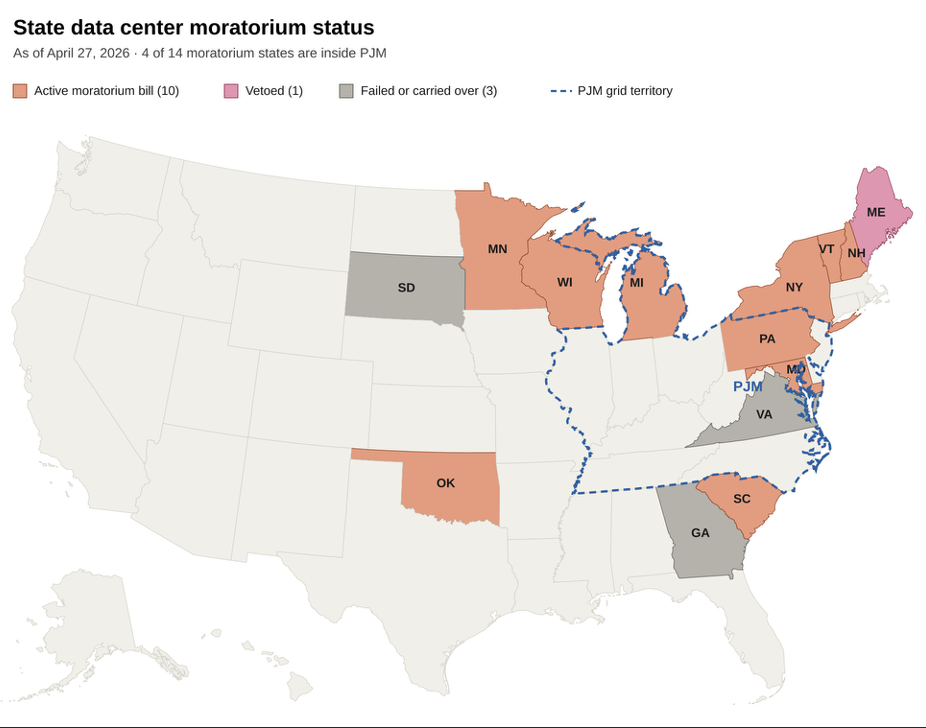

Fourteen states have moratorium activity in the 2026 session. Ten bills are alive: Maryland, Michigan, Minnesota, New Hampshire, New York, Oklahoma, Pennsylvania, South Carolina, Vermont, and Wisconsin. Maine vetoed last week. Three failed or carried over: Georgia, South Dakota, Virginia. Sens. Bernie Sanders and Rep. Alexandria Ocasio-Cortez introduced a federal moratorium in March.

Four of the fourteen sit inside PJM – the regonal transmission organization (RTO) that manages the high voltage grid for 65 million people across 13 states. Here is what that count understates: Maryland, Michigan, Pennsylvania, and Virginia host roughly 570 operating data centers. Another 287 are planned in Virginia alone, per Pew Research using Data Center Map. So, 1 in 7 of the US footprint are sitting under bills that would freeze development.

The states in PJM are leaning toward frameworks over freezes: Pennsylvania’s HB 1834, Maryland’s co-location-with-generation requirement, and Illinois’s POWER Act. It’s a nuance that tracks closer to experience. However, someone needs to explain more to the PJM ratepayers who have lived with the auction pain. With better understanding and aligned (as in not lopsided) incentives, I think they’d opt for the developer to pay, not the developer to leave.

Maine is the cautionary tale. Governor Janet Mills vetoed LD 307 last week over a Jay carveout that the legislature refused. She signed the companion bill LD 713, removing data centers from state business tax incentive programs.

On the other end of the policy menu sits the federal answer. Trump’s Ratepayer Protection Pledge, signed March 4 by Amazon, Google, Meta, Microsoft, OpenAI, Oracle, and xAI, is voluntary. It has no enforcement. The three largest data center projects in Arizona are being built by companies that did not sign. A handshake from seven hyperscalers does not bind the next 200 developers.

The receipts

Three numbers explain why the moratoriums are appearing. They also explain why a moratorium doesn’t fix any of them.

One. PJM’s capacity auction price went from $28.92 per megawatt-day in 2024 to $329.17 in the 2026/2027 auction, hit the FERC-approved cap of $333.44 in the December 2025 auction, and, for the first time in PJM history, fell 6,623 MW short of the reliability requirement. PJM’s Independent Market Monitor attributed 40% of the $16.4 billion in cleared costs, or $6.5 billion, to data center load. That’s not just unprecedented, it’s painful.

Two. Union of Concerned Scientists analysis found utilities in seven PJM states passed $4.36 billion in data center grid connection costs to all ratepayers in 2024. Six of 130 projects were paid for by the data centers themselves. The other 124 were socialized. Pennsylvania ratepayers absorbed $492 million.

Three. Water. Shaolei Ren’s April 2026 paper, “Small Bottle, Big Pipe,” puts US data center water needs at 697 to 1,451 million gallons per day of new public water capacity by 2030, equivalent to New York City’s daily supply. Public infrastructure cost: $10 to $58 billion.

So, we need a moratorium because governments and utilities have not been able to deliver in ways that benefited their constituents. In other words, they didn’t do their work, so now all work has to stop?

Islanding: who benefits? Operators but less so the states

Alex Lanin’s March 22 brief re: Illinois deserves attention. ComEd’s residential capacity charge jumped from $0.91/month in mid-2024 to $8.00/month by mid-2025, a 775% increase. Illinois has 220-plus operating data centers, 3,900 MW in the planning pipeline, and over 75 ComEd interconnection applications totaling more than 28 GW. Statewide electricity costs rose 15% between 2024 and 2025 against a 4.5% national average. Since 2019, Illinois has issued $983 million in tax breaks across 27 facilities.

The math is right. In my opinion, the prescription is wrong.

The Illinois POWER Act builds around what supporters call BYONCCE: Bring Your Own New Clean Capacity and Energy. Data centers that secure 80% of their power from new clean energy by 2030 receive fast-track interconnection - those who do not wait in the general queue. I love the clean energy angle.

Yet, islanding in sustainability paint doesn’t address the public grid bearing connection upgrade costs. The municipality still pays for the substation. Neighbors foot the transmission bill. And when the grid needs flexibility on a hot day, the data center, behind its own meter, adds nothing to the system the rest of us share. I’m not feeling that benefits equally.

You do not fix a grid by pulling capacity out of it. You fix it by adding flexibility. The build-a-moat model is great for the developer. It is a worse outcome for the locality, because the host geography gets the substation, the noise, the water draw, and none of the grid resilience.

What does curtailment actually mean?

Twenty to thirty percent of the load sounds aggressive. It is not, but you gotta read the math correctly.

Duke University researchers found that if data centers nationwide could limit their power use during just the top few hours of peak grid demand each year, the US grid could accommodate roughly 100 gigawatts of additional data center load without building new power plants. The required annual curtailment rate: 0.5 to 1%. That is 50 to 200 hours per year, on the hottest, most stressed days. RMI puts it more bluntly: at 0.5%, the freed capacity is equivalent to about 1,000 hyperscale data centers, roughly double what is in the pipeline today. (I’m not an engineer, so if I have this math wrong, please sort me out.)

What the curtailment looks like during those hours: in May 2025, NVIDIA, Oracle, the Salt River Project, and EPRI ran a demonstration in Phoenix. The data center reduced its power draw by 25%. The reduction held for three hours. The AI workload finished without disruption. Software-based workload orchestration shifted training jobs and synchronized checkpoints to ride out the grid stress event. Published in Nature Energy. First peer-reviewed validation of data center demand flexibility at commercial scale. It’s one of the reasons why digital twins show so much promise. Being able to model these things in advance and near the real-time event delivers flexible new paths that allow better service to all stakeholders.

So, the realistic policy ask is not run at 70% all the time. It is: 50 to 200 hours per year, expect a 20 to 30% reduction in draw, sustained for two to four hours per event, with notice. That is the difference between 100 GW of new grid capacity and three more gas peakers per region.

Batteries can do most of the work

Before a data center must slow training jobs, it should have batteries. Two kinds, doing two different jobs. (I’ve said it before – I am a battery fangirl. It’s weird, I know.)

Behind-the-meter BESS is the data center’s own storage, sized to the facility. It absorbs the second-by-second power swings of large AI training jobs, which fluctuate by hundreds of megawatts within seconds during synchronized GPU phases, without those swings reaching the grid. It also lets the facility shift load away from peak hours, peak-shave to avoid demand charges, and respond to grid signals without interrupting compute (there’s a lot of techno babble there – it’s about smoothing out load balance, roughly speaking).

Front-of-the-meter BESS is utility-scale storage, paid for or co-funded by the developer, sited where the public grid needs the support. It adds capacity to the system the localitydepends on. It earns revenue across ancillary services, frequency regulation, peak shaving, and the wholesale capacity market. It is the opposite of an island.

Real proof of concept. In Hillsboro, Oregon, Aligned Data Centers signed a deal with Portland General Electric and Calibrant for a 30 MW / 60 MWh battery that let the campus interconnect years earlier than traditional utility upgrades would have allowed. The battery is the reason the data center is online at all. EPRI’s DCFlex initiative aims to deploy five to ten flexibility hubs of this kind by 2027.

A state framework should require both. BTM BESS sized to the facility’s peak power swings, as a condition of permitting. FTM BESS, co-funded by the developer at a defined ratio of MW capacity, contributed to the public grid as the price of front-of-queue interconnection. The combined effect: less stress on the grid and more capacity in it. Capacity addition, not capacity escape.

On tax breaks. Asking for a friend.

Do data centers really need them?

For years, states answered yes. They cited a 2022 University of Georgia study finding that 90% of Georgia’s data center activity was attributable to the state’s tax exemption. That number was the rationale for $1 billion-a-year giveaways in Texas, $732 million a year in Virginia, and $983 million in cumulative breaks to 27 facilities in Illinois.

Then the same University of Georgia team published a 2025 update. The revised number: 30%. Seventy percent of the activity would have occurred without the tax break. Tim Bartik of the Upjohn Institute puts the share of firms making location decisions on incentives at 2 to 25% across industries. Georgia State Sen. Chuck Hufstetler, a Republican, said the quiet part out loud: “It’s a competition of who can build it the quickest. It’s more important to them that they’re built first versus the cost.”

Good Jobs First found that 10 states are losing more than $100 million a year on data center incentive programs. Twelve states do not even disclose what they are losing. Pennsylvania’s data center sales tax exemption is projected at $2 billion in foregone revenue by 2031.

Asking for a friend: if 70% of the activity is going to happen anyway, what is the tax break buying?

Two answers, depending on whether you keep it.

If you keep it, condition it. Demand response participation. BTM and FTM BESS commitments. Community benefit agreements before the credit unlocks. Bill relief fund contributions. Peak-water reporting. Heat reuse where geography permits. The break stops being a giveaway and becomes a lever. The state captures the community returns that were going to be left on the table.

If you cap or repeal it, redirect the recovered revenue into the costs the data centers are generating against: bill relief, grid resilience investments, water infrastructure, and workforce training. Washington State and Arizona have moved in that direction. Michigan repealed its 2024 incentive. Illinois’s Pritzker has reversed.

Pennsylvania has a $2 billion choice in front of it. The legislature should not let that exemption renew without conditions attached. Either the developer pays the locality back, or the locality keeps the money.

We don’t need a moratorium – we need revenue recapture.

The framework I want

The full policy stack a state should write:

• Annual curtailment commitment of 0.5 to 1% of uptime, with per-event reductions of 20 to 30%, sustained for 2 to 4 hours, on grid operator notice

• BTM BESS sized to absorb facility-level power swings, as a condition of permitting

• FTM BESS co-funded by the developer at a defined MW ratio, contributed to the public grid as the price of front-of-queue interconnection

• Conditional tax incentive, or none, with demand response, BESS, and community benefit agreements as the unlock

• Peak-water reporting modeled on Ren’s standard, with dry-cooling protocols when community water systems are stressed

• Heat reuse requirements for adjacent industrial or district energy where geography supports it

• Bill relief funds seeded by demand response payments, returning dollars to elderly residents on fixed incomes who pay the same rate increases as everyone else

That last point is not philanthropy. It is value recapture for the people who host the infrastructure.

Across a 100 MW facility lifecycle, the difference between the island model and the participating model runs $150 to $270 million in combined incentives, avoided costs, capacity payments, and grid services revenue. The participating model is not the good-citizen option. It is the better business. A developer who maps these overlapping incentives first has a structural cost advantage that compounds across every subsequent site.

Pennsylvania can go first

Governor Shapiro is not wrong about the inputs. Pennsylvania has the energy infrastructure, the research institutions, the labor supply, and the regulatory environment. That is not why $100 billion in private AI investment has been announced in the last year. That is the table stakes. The competition is over the framework.

His GRID standards in February, transparency, community outreach, water conservation, local hiring, are the right instincts. Instincts are not a framework.

HB 1834 passed the House in March. It moves in the right direction. So does HB 2151. Sen. Muth’s three-year hyperscale moratorium memo moves in the wrong direction. The state with a freeze does not lose only the facility under review. It loses the supply chain, the workforce program, the energy park, the base load anchor, and the permitting speed on the next site.

I want Pennsylvania to write the framework. Curtailment commitment with realistic numbers. BTM and FTM BESS as conditions of permitting. Tax incentive only on those terms, or repealed. Community benefit agreements before any state credit unlocks. Peak-water reporting. A bill relief fund seeded by demand response payments.

The moratorium is the response of a state that has not decided what it wants. The framework is the response of a state that knows. The next data center, sited in Pennsylvania on those terms, will be the proof of concept. The one after that will be faster. The one after that will be invited.

Frequently asked questions

Is curtailing 20 to 30% of a data center’s load realistic?

It is, if the curtailment happens 50 to 200 hours per year and lasts two to four hours per event. Duke University research shows a 0.5 to 1% annual curtailment rate would unlock about 100 GW of new grid capacity. NVIDIA, Oracle, and EPRI ran a Phoenix demonstration in May 2025 that achieved a 25% reduction sustained for three hours with no AI workload disruption. Published in Nature Energy.

What is wrong with bring-your-own-power and BYONCCE?

It is islanding dressed in clean energy. The developer builds dedicated generation and pulls load off the public grid. The locality hosts the infrastructure and gets none of the flexibility. Capacity escape does not improve grid resilience. Demand response and BESS do.

Why require both BTM and FTM batteries?

BTM (behind-the-meter) handles the facility’s second-by-second power swings, peak shaving, and demand response participation without interrupting compute. FTM (front-of-the-meter) is utility-scale storage that adds capacity to the public grid. The Aligned data center in Hillsboro, Oregon, used a 30 MW / 60 MWh BESS to interconnect years earlier than traditional utility upgrades would have allowed. EPRI’s DCFlex initiative is deploying 5 to 10 flexibility hubs by 2027.

Do data centers really need state tax incentives?

Probably not, or not at the scale states are giving them. The 2022 University of Georgia study claimed 90% of Georgia’s data center activity was due to the incentive. The 2025 University of Georgia update revised that to 30%. Tim Bartik’s research puts the typical incentive-driven share at 2 to 25%. If states keep the breaks, the breaks should be conditioned on demand response, BESS, and community benefit agreements. If they do not condition them, they should repeal them.

How many data centers sit under PJM moratorium pressure?

Roughly 570 operating facilities across Maryland, Michigan, Pennsylvania, and Virginia, plus another 287 planned in Virginia alone. Approximately one in seven of the US footprint.

Appendix: state moratorium bills

Bill numbers, key terms, and current status. As of April 27, 2026.

Active bills (10):

• Maryland — HB 120. (In PJM.) No new approvals until the General Assembly enacts a co-location-with-generation framework, including gas, nuclear, or SMR.

• Michigan — statewide bill + HR 240. (In PJM.) Statewide proposal plus HR 240. At least 19 Michigan communities have local moratoriums.

• Minnesota — SF 4298. No state or local data center permits until one year after the PUC submits a comprehensive impact study.

• New Hampshire — HB 1265. One-year construction freeze plus a study committee.

• New York — S9144 / A10141. Three-year moratorium on facilities above 20 MW. Stalled in committee since February.

• Oklahoma — SB 1488. Moratorium until November 1, 2029, while the Corporation Commission studies water, rates, property values, and siting.

• Pennsylvania — Muth memo + HB 1834. (In PJM.) Sen. Katie Muth filed a three-year hyperscale moratorium memo. HB 1834 (BYO clean energy framework) and HB 2151 (state model ordinance) passed the House in March.

• South Carolina — H. 5286. Joint resolution barring state and local permits, approvals, or incentives until January 1, 2028.

• Vermont — S.205. Moratorium on AI data centers above 100 MW through July 2030. Longest proposed window in the country.

• Wisconsin — LRB-6377/1. Moratorium until the legislature enacts a planning authority and bans on shifting data center costs to residential customers.

Vetoed (1):

• Maine — LD 307. Vetoed by Gov. Mills on April 24, 2026 over a Jay carveout the legislature refused. LD 713 (no business tax incentives for data centers) was signed.

Failed or carried over (3):

• Georgia — HB 1012, SB 410, SB 408. All three failed when the Senate adjourned.

• South Dakota — SB 232. Failed. SB 135 passed, giving local governments authority to regulate or ban data centers themselves.

• Virginia — HB 1515. (In PJM.) Carried over to 2027. HB 2084 (rate classification review) was enacted.

Federal:

• S.4214 / House companion. AI Data Center Moratorium Act introduced March 2026 by Sen. Bernie Sanders and Rep. Alexandria Ocasio-Cortez.

I write about energy, AI, infrastructure, and the decisions shaping local economies. Follow for more analysis. Get in touch if I can help with your thought leadership, offers, or comms.